For solar developers and financiers, PM KUSUM Component A is not just a capex-and-yield problem. It is a cash-collection problem. When your offtaker is a DISCOM, the project�s �real� revenue is not the tariff on paper�it�s the tariff collected on time, with minimal disputes, and with enforceable payment security.

This is where DISCOM Credit Risk in KUSUM-A becomes the single most important bankability variable�often more critical than module brand, tracker choice, or even marginal differences in CUF.

Key takeaways :-

DISCOM Credit Risk in KUSUM-A is the probability that invoices are delayed, disputed, or partially paid, reducing usable cashflows for debt service and equity returns.

Decentralized solar under PM KUSUM Component A often has higher friction in metering, billing, and approvals�amplifying collection risk.

The same nominal tariff can produce very different IRRs depending on payment delays and working capital financing costs.

Bankable structures typically use a stack: LC + escrow + clear invoicing protocol + enforcement rights (and, where possible, state support).

Receivable monetization (bill discounting/factoring) can protect liquidity, but only works when receivables are clean, assignable, and undisputed.

DISCOM Credit Risk in KUSUM-A is the probability that invoices are delayed, disputed, or partially paid, reducing usable cashflows for debt service and equity returns.

Decentralized solar under PM KUSUM Component A often has higher friction in metering, billing, and approvals�amplifying collection risk.

The same nominal tariff can produce very different IRRs depending on payment delays and working capital financing costs.

Bankable structures typically use a stack: LC + escrow + clear invoicing protocol + enforcement rights (and, where possible, state support).

Receivable monetization (bill discounting/factoring) can protect liquidity, but only works when receivables are clean, assignable, and undisputed.

DISCOM Credit Risk in KUSUM-A refers to the likelihood that the DISCOM, as the power purchaser, may fail to meet its payment obligations in full and on time�thereby creating uncertainty in the project�s receivables and cash flows. This risk is particularly relevant given the varying financial health of state DISCOMs and their historical payment delays. If not properly mitigated through contractual and financial safeguards, DISCOM credit risk can directly impact project bankability, debt servicing ability, and overall investor confidence in KUSUM-A solar projects.

In practical terms, it shows up as:

Payment delays: invoices cleared in 60�180+ days instead of 30�45 days

Part-payments: intermittent releases that don�t match billed amounts

Deductions and disputes: meter-reading disputes, adjustment entries, or �pending approvals�

Procedural bottlenecks: delays in bill acceptance, energy accounting, and internal DISCOM workflows

Policy and fiscal stress: delayed subsidy reimbursement to DISCOMs can spill into generator payments

Payment delays: invoices cleared in 60�180+ days instead of 30�45 days

Part-payments: intermittent releases that don�t match billed amounts

Deductions and disputes: meter-reading disputes, adjustment entries, or �pending approvals�

Procedural bottlenecks: delays in bill acceptance, energy accounting, and internal DISCOM workflows

Policy and fiscal stress: delayed subsidy reimbursement to DISCOMs can spill into generator payments

A PPA can be technically valid and fully compliant on paper, yet still generate weak or unpredictable cash flows if the billing, verification, and payment cycles are unstable or delayed. For lenders and investors, DISCOM Credit Risk in KUSUM-A receivables are only as dependable as the robustness of the enforcement framework and the payment-security architecture�such as escrow mechanisms, guarantees, letters of credit, and clearly defined cure periods�standing behind them. Weak implementation of these safeguards can materially increase perceived risk, affect financing terms, and ultimately erode project returns.

DISCOM Credit Risk in KUSUM-A tends to be structurally higher than in many large utility-scale PPAs because decentralized plants multiply interfaces, approvals, and operational dependencies. Each project is linked to local substations, feeder-level metering, land aggregation, and state-level DISCOM processes, increasing the chances of administrative delays and coordination gaps. As a result, payment timelines are more exposed to operational bottlenecks and local governance issues, making cash flows less predictable unless strong contractual and payment-security mechanisms are in place.

Key drivers:

1) Small-ticket invoices get lower institutional priority

A 0.5�2 MW plant invoice is operationally �small� for many DISCOM finance teams�especially versus bulk procurement, transmission charges, or legacy payment obligations.

2) Metering, energy accounting, and feeder-level complexity

Decentralized injection points increase the probability of:

meter-reading errors or delayed readings

disputes on export/import netting (where applicable)

delays in joint meter verification or testing certificates

dependency on local field staff bandwidth and accountability

meter-reading errors or delayed readings

disputes on export/import netting (where applicable)

delays in joint meter verification or testing certificates

dependency on local field staff bandwidth and accountability

3) Rural operational constraints create administrative drag

Remote locations can cause longer turnaround times for:

breakdown rectification sign-offs

inspection closures

commissioning and synchronization documentation

These don�t just affect COD�they affect steady-state billing.

breakdown rectification sign-offs

inspection closures

commissioning and synchronization documentation

These don�t just affect COD�they affect steady-state billing.

4) Subsidy economics and political economy

DISCOM payment behavior is ultimately tied to liquidity, subsidies, and state fiscal health. That context matters for renewable energy financing India because lenders underwrite cashflow reliability, not just policy intent.

When DISCOM Credit Risk in KUSUM-A rises, the project doesn�t just �feel� riskier�it becomes measurably less financeable unless pricing and structure adjust.

A quick mapping of where the risk lands

Solar tariff risk: the �unpriced� problem

In many state programs, tariffs are implicitly expected to remain competitive and low. But solar tariff risk emerges when developers cannot fully price in collection uncertainty. Result: projects look viable on paper and weak in cashflow reality.

The working-capital math investors actually care about

If invoices are paid 120 days late rather than 45 days, the project must fund ~75 additional days of receivables. That is not accounting noise; it is:

incremental interest cost

lower free cash for distributions

higher probability of covenant stress in weak months

incremental interest cost

lower free cash for distributions

higher probability of covenant stress in weak months

A bankable KUSUM-A structure usually combines multiple tools. Relying on one instrument alone is rarely sufficient for high-quality financing outcomes. Instead, lenders and investors look for layered risk mitigation�such as escrow accounts, letters of credit, state guarantees, and clearly defined default and cure mechanisms�working together in a coordinated framework. This multi-layered approach improves payment certainty, strengthens lender confidence, and helps achieve better debt terms, lower risk premiums, and more sustainable long-term project cash flows.

Summary of common payment-security instruments

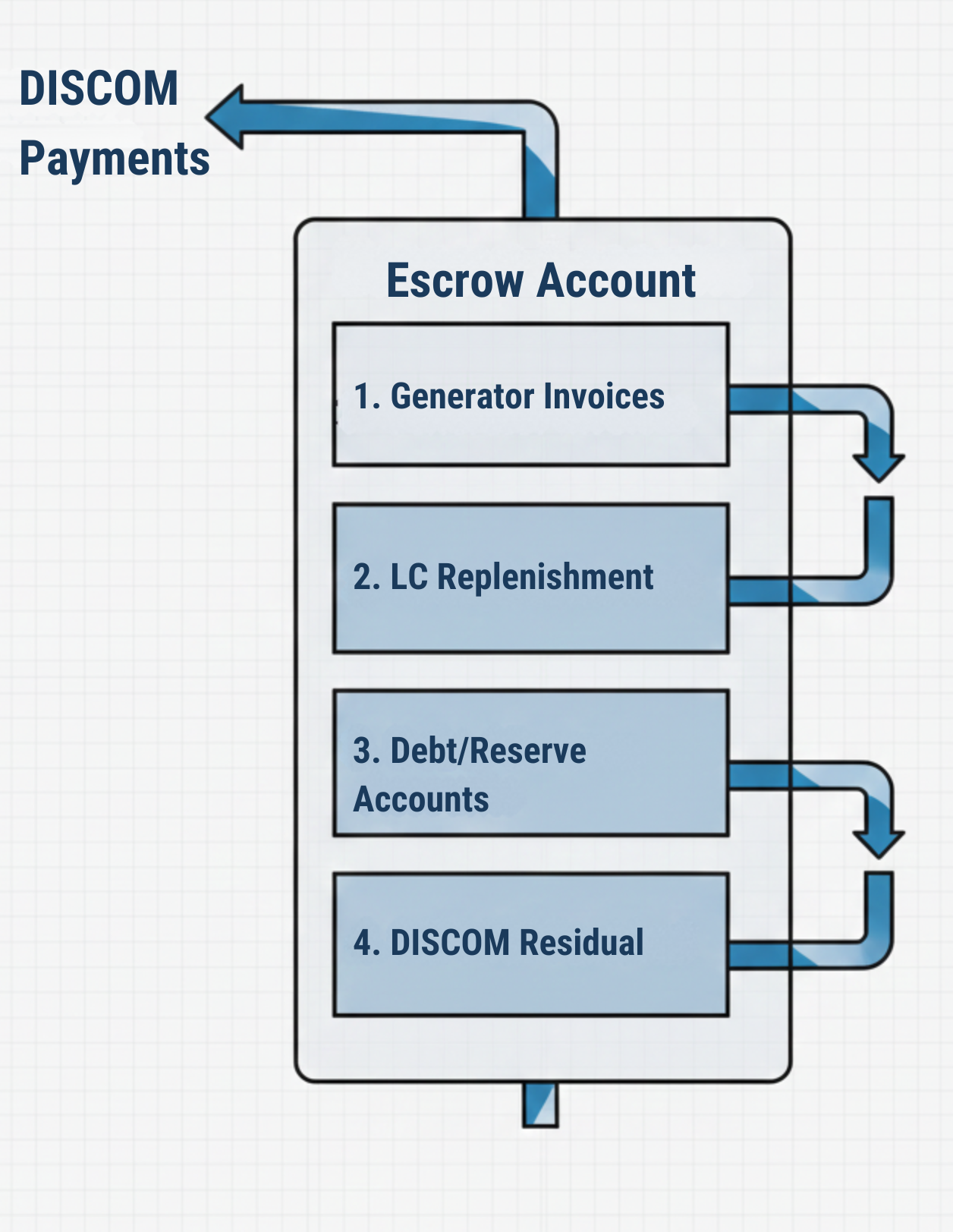

An escrow is meant to ring-fence cash so that power payments are not competing with every other DISCOM obligation. By creating a dedicated, controlled payment waterfall�typically funded from identified revenue sources�it ensures that DISCOM Credit Risk in KUSUM-A power payments are prioritized and insulated from the DISCOM�s broader liquidity pressures. This structure reduces payment delays, improves predictability of cash flows, and enhances overall lender comfort with the project�s receivables.

How an escrow mechanism typically works

DISCOM (or a designated account) routes specified revenues into an escrow account.

A waterfall prioritizes payment of power invoices (and sometimes LC replenishment) before other uses.

If triggers are met (e.g., overdue days), the project/lenders can instruct the bank to release funds per waterfall.

DISCOM (or a designated account) routes specified revenues into an escrow account.

A waterfall prioritizes payment of power invoices (and sometimes LC replenishment) before other uses.

If triggers are met (e.g., overdue days), the project/lenders can instruct the bank to release funds per waterfall.

What to negotiate for KUSUM-A receivables

Clearly defined funding source: which revenues feed the escrow

Waterfall priority: generator payments ahead of non-essential outflows

Triggers and cure periods: when the waterfall �tightens�

Control and access: who can instruct the escrow bank (especially on default)

Clearly defined funding source: which revenues feed the escrow

Waterfall priority: generator payments ahead of non-essential outflows

Triggers and cure periods: when the waterfall �tightens�

Control and access: who can instruct the escrow bank (especially on default)

Limitations in decentralized contexts

Escrows fail when they are:

underfunded or inconsistently funded

structured without clear control rights

politically overridden in stress periods

This is why DISCOM Credit Risk in KUSUM-A is mitigated best when escrow is paired with an LC and enforceable remedies.

underfunded or inconsistently funded

structured without clear control rights

politically overridden in stress periods

This is why DISCOM Credit Risk in KUSUM-A is mitigated best when escrow is paired with an LC and enforceable remedies.

A properly designed LC is often the most effective short-term shield against DISCOM payment risk, as it provides an assured and time-bound source of payment independent of the DISCOM�s immediate cash position. By enabling automatic drawdown in case of payment delays, an LC improves receivable certainty, strengthens lender confidence, and reduces short-term liquidity stress for the project�especially during the early years of operation when cash flows are most sensitive.

What makes an LC bankable

A strong LC escrow mechanism stack usually includes:

Irrevocable, revolving LC issued by a credible bank

Coverage of 1�3 months of expected invoices (project-specific)

Clear invocation process and documentary requirements

Auto-replenishment obligation tied to DISCOM timelines

PPA clauses preventing unilateral LC reduction without consent

Irrevocable, revolving LC issued by a credible bank

Coverage of 1�3 months of expected invoices (project-specific)

Clear invocation process and documentary requirements

Auto-replenishment obligation tied to DISCOM timelines

PPA clauses preventing unilateral LC reduction without consent

Where LCs fail in real projects

LC is issued but not renewed on time

Documentary requirements are overly complex, causing invocation friction

LC amount is too small versus actual billing cycle

DISCOM disputes invoices, slowing invocation or settlement

LC is issued but not renewed on time

Documentary requirements are overly complex, causing invocation friction

LC amount is too small versus actual billing cycle

DISCOM disputes invoices, slowing invocation or settlement

For lenders, a robust LC is often the difference between �financeable with standard covenants� and �needs higher equity + tighter cash controls.�

In many Indian power contracts, tripartite arrangements aim to reduce discretion and increase enforceability.

What a KUSUM-A tripartite should achieve

A workable tripartite agreement (typically among the DISCOM, state government, and the project company and/or lenders) should define:

payment responsibility and timeline

consequences of persistent delays

practical enforcement, including set-off from defined state flows where applicable

lender step-in and assignment recognition for KUSUM-A receivables

payment responsibility and timeline

consequences of persistent delays

practical enforcement, including set-off from defined state flows where applicable

lender step-in and assignment recognition for KUSUM-A receivables

Tripartite agreements help when they are designed as operational enforcement tools�not ceremonial add-ons.

A credible state guarantee can materially reduce DISCOM Credit Risk in KUSUM-A, especially where DISCOM finances are stressed.

What financiers look for in state-backed structures

Unconditional, irrevocable payment guarantee (not �best effort�)

Clear invocation conditions (time-based, not judgment-based)

Defined payment timelines post-invocation

Budgetary appropriation and legal enforceability

Unconditional, irrevocable payment guarantee (not �best effort�)

Clear invocation conditions (time-based, not judgment-based)

Defined payment timelines post-invocation

Budgetary appropriation and legal enforceability

Reality check: guarantee quality varies

State support is not uniform. For state guarantee power projects, the practical value depends on:

how quickly obligations are honored

whether the guarantee is designed for automatic payment vs prolonged claims

whether the DISCOM has historically relied on ad hoc releases

how quickly obligations are honored

whether the guarantee is designed for automatic payment vs prolonged claims

whether the DISCOM has historically relied on ad hoc releases

For KUSUM-A, the best use of a guarantee is to lower the risk premium and unlock better debt terms�rather than to replace operational payment discipline.

The central role in PM KUSUM Component A is primarily programmatic: guidelines, funding support structures, and implementation oversight through MNRE and state agencies.

From a receivables perspective:

Central involvement can improve standardization and encourage payment-security norms.

However, central program participation is not the same as a sovereign guarantee of DISCOM payments.

Central involvement can improve standardization and encourage payment-security norms.

However, central program participation is not the same as a sovereign guarantee of DISCOM payments.

This distinction matters: lenders will still underwrite DISCOM Credit Risk in KUSUM-A based on offtaker behavior and enforceable security, not policy intent.

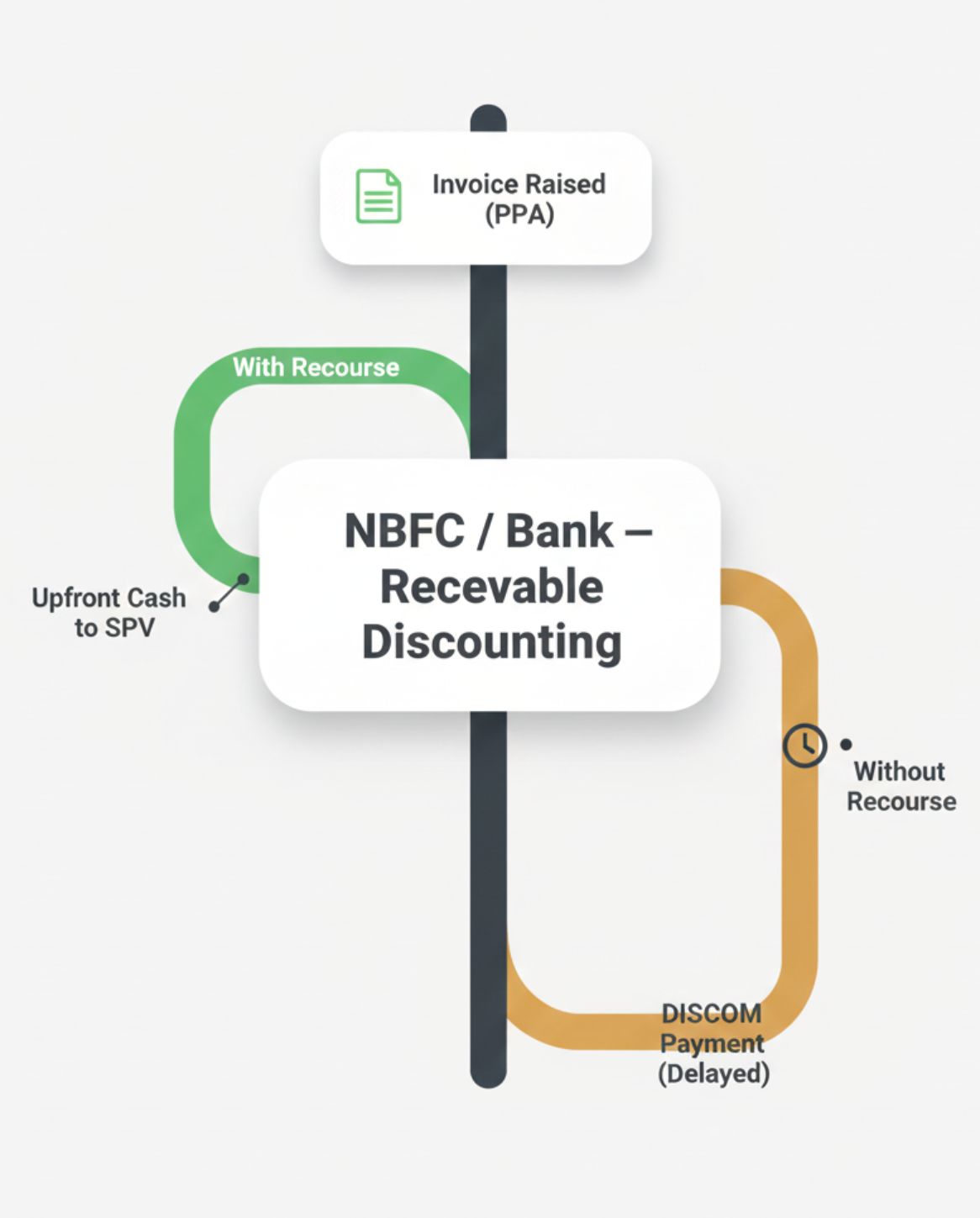

When delays persist, developers often turn to receivable discounting solar structures, converting approved invoices into near-term cash to ease liquidity pressure. In India, this is typically done through RBI-regulated TReDS platforms, as outlined on official RBI and Ministry of Power websites, helping reduce working-capital stress from DISCOM payment delays.

How receivable discounting works (typical structure)

Project company raises invoices per PPA.

A bank/NBFC discounts those receivables and pays an agreed percentage upfront.

On DISCOM payment, the financier gets repaid (with fees/interest).

Can be with recourse (developer bears default risk) or without recourse (costlier and rarer).

Project company raises invoices per PPA.

A bank/NBFC discounts those receivables and pays an agreed percentage upfront.

On DISCOM payment, the financier gets repaid (with fees/interest).

Can be with recourse (developer bears default risk) or without recourse (costlier and rarer).

What makes KUSUM-A receivables discountable

Discounting is practical only when:

invoices are accepted with minimal disputes

receivables are assignable and recognized in documentation

payment flows are predictable enough to price the facility

invoices are accepted with minimal disputes

receivables are assignable and recognized in documentation

payment flows are predictable enough to price the facility

Factoring is a tool for liquidity�not a cure for weak offtaker discipline. Still, for portfolios, receivable programs can materially reduce �cashflow whiplash� and improve construction-to-operations stability.

Lenders price DISCOM Credit Risk in KUSUM-A through a combination of:

higher spread / margin over base rates

stricter DSCR requirements

lower leverage (higher equity share)

stronger cash controls (escrow, DSRA, cash sweep triggers)

tighter conditions precedent (CPs) to first disbursement

higher spread / margin over base rates

stricter DSCR requirements

lower leverage (higher equity share)

stronger cash controls (escrow, DSRA, cash sweep triggers)

tighter conditions precedent (CPs) to first disbursement

Risk premium in tariffs: what it really compensates

A tariff risk premium often compensates for:

higher working capital interest

expected delay variability (not just average delay)

probability-weighted �tail� events (multi-quarter non-payment)

higher working capital interest

expected delay variability (not just average delay)

probability-weighted �tail� events (multi-quarter non-payment)

If tariffs are capped, the adjustment moves elsewhere: higher equity, lower debt, or refusal to bid.

Impact on WACC and DSCR

WACC rises when debt becomes more expensive and equity requires a higher return for liquidity stress.

DSCR constraints tighten when lenders assume conservative collections or force additional reserves.

WACC rises when debt becomes more expensive and equity requires a higher return for liquidity stress.

DSCR constraints tighten when lenders assume conservative collections or force additional reserves.

Conservative vs aggressive structuring

If you want competitive financing, treat DISCOM Credit Risk in KUSUM-A as a design variable from day one�not a post-award inconvenience.

What developers should negotiate (PPA + security package)

Prioritize clauses and instruments that reduce discretion:

Payment timeline + late payment surcharge with clear calculation method

Bill acceptance protocol: meter reading, joint verification, dispute window

LC terms: amount, renewal timelines, replenishment triggers, invocation documents

Escrow waterfall: funding source, payment priority, bank control rights

Assignment recognition: lender�s right to receive payments on default

Cure periods and remedies: what happens if delays exceed defined thresholds

Change-in-law and regulatory risk allocation: avoid open-ended deductions

Payment timeline + late payment surcharge with clear calculation method

Bill acceptance protocol: meter reading, joint verification, dispute window

LC terms: amount, renewal timelines, replenishment triggers, invocation documents

Escrow waterfall: funding source, payment priority, bank control rights

Assignment recognition: lender�s right to receive payments on default

Cure periods and remedies: what happens if delays exceed defined thresholds

Change-in-law and regulatory risk allocation: avoid open-ended deductions

What lenders and NBFCs typically look for

DISCOM historical payment behavior (to generators and within the state ecosystem)

robustness of payment security (LC + escrow)

clarity of invoicing and metering protocol

enforceability of assignment and step-in rights

portfolio approach: diversified offtaker exposure reduces single-node risk

DISCOM historical payment behavior (to generators and within the state ecosystem)

robustness of payment security (LC + escrow)

clarity of invoicing and metering protocol

enforceability of assignment and step-in rights

portfolio approach: diversified offtaker exposure reduces single-node risk

FAQ's

DISCOM Credit Risk in KUSUM-A is the risk that the DISCOM delays, disputes, or fails to pay KUSUM-A invoices on time, reducing usable project cashflows for debt and equity.

Delays increase receivable days and force developers to fund working capital via equity or short-term debt, which reduces distributable cash and compresses equity IRR even if the tariff is unchanged.

An LC is usually the strongest first-line protection for near-term invoices, while escrow improves structural discipline. The best outcomes typically come from combining LC + escrow with clear invoicing and enforcement rights.

Financiers generally prefer LC cover that matches a realistic billing-to-payment cycle (often multiple invoice periods). The right level depends on metering timelines, DISCOM payment history, and the PPA�s invocation and replenishment clauses.

Yes, but financing quality depends on the strength of payment security and cash controls (LC/escrow), plus conservative assumptions on receivable days. Weak security often leads to lower leverage and higher equity requirements.

Typical dispute triggers include meter-reading delays, joint meter verification gaps, energy accounting reconciliation issues, documentation mismatches, and administrative approval delays inside DISCOM billing workflows.

They price it through higher spreads, stricter DSCR and covenant packages, lower leverage, and additional reserves (DSRA/working capital buffers). Strong payment security can reduce the risk premium materially.

Receivable discounting solar is invoice financing where a bank/NBFC advances cash against DISCOM invoices and gets repaid on collection. It works best when invoices are clean, accepted, assignable, and payment behavior is predictable.

Use a structured lens: historical payment delays to generators, ACS�ARR gap, AT&C losses, liquidity support patterns, and evidence of LC/escrow compliance. Pair this with direct market feedback from lenders active in that state.

Not always. If the program or state has tariff ceilings, risk may need to be managed through structure (LC, escrow, guarantees, receivable facilities) and conservative leverage rather than only through tariff escalation.